В этой стране более 400 000 страховых агентов, и почти все они хотели бы продать вам полный полис страхования жизни. Если вы покупаете полис со страховыми взносами в размере 40 000 долларов США в год, комиссия для этого агента обычно составит от 20 000 до 44 000 долларов США. Как вы можете себе представить, эта комиссия может быть очень мотивирующей, особенно учитывая средний доход страхового агента в 49 840 долларов. Что еще хуже, многие из худших полисов предлагают самые высокие комиссии. К сожалению, подавляющее большинство продаваемых полисов продаются ненадлежащим образом, и подавляющее большинство тех, кто их продает, являются продавцами, маскирующимися под финансовых консультантов.

В результате этого нелепого конфликта интересов агенты часто могут выдвигать серьезные мифы, пытаясь убедить вас купить их продукт, что может объяснить печальную статистику о том, что более 80% тех, кто покупает этот продукт, избавляются от него перед смертью, а опросы реальных врачей на этом сайте и в нашей группе в Facebook показывают, что подавляющее большинство из тех, кто приобрел полисы на всю жизнь, сожалеют о своей покупке. Если для вас это новость, прочтите «Все, что вам нужно знать о страховании жизни», прежде чем продолжить этот пост.

Хотя большинство членов группы WCI в ФБ никогда не приобретали страховку на всю жизнь, 76% из тех, кто сделал это, сожалеют об этом.

Загрузка...

Цифры аналогичны, но немного ниже в текущем опросе на этом сайте (который, в отличие от группы FB, позволяет голосовать тем, кто продает эти полисы).

Многие думают, что я ненавижу страхование всей жизни. Я на самом деле нет. Я ненавижу то, как оно продается, и тех, кто продает его ненадлежащим образом. Если вы действительно понимаете, как это работает, и все еще хотите этого, то смело покупайте столько, сколько захотите. На меня это действительно не влияет так или иначе. Но мне надоело сталкиваться с читателями и слушателями, которые НЕ ПОНИМАЛИ, как это работало, когда покупали, а как только они это понимают, НЕ ХОТЯТ этого.

Страхование всей жизни можно оформить разными способами, но, как правило, вы платите ежемесячный или ежегодный взнос либо в течение определенного периода времени, либо до тех пор, пока не умрете. Чем дольше период времени, в течение которого вы платите страховые взносы, тем ниже размер страховых взносов. Всякий раз, когда вы умираете, ваш бенефициар получает доходы от полиса. Поскольку каждый полис страхования жизни гарантированно выплачивается, если вы просто будете держать его до самой смерти, страховые взносы намного выше, чем по сопоставимому полису срочного страхования жизни.

Полис полного страхования жизни, как и другие виды постоянного страхования жизни, на самом деле представляет собой гибрид страхования и инвестиций. Полис накапливает денежную стоимость с течением времени. Эта денежная стоимость растет без уплаты налогов, и вы даже можете занять эти деньги без налогов (но не без процентов). После вашей смерти все, что вы взяли в долг (плюс проценты), вычитается из пособия по случаю смерти, а остальная часть выплачивается вашему бенефициару. (Вы получаете денежную стоимость или пособие в случае смерти, а не то и другое.)

Этот инвестиционный аспект позволяет тем, кто продает страхование жизни, находить всевозможные творческие причины, по которым вам следует его купить, и творческие способы его структурирования. Самые ярые сторонники могут даже утверждать, что вам не нужны НИКАКИЕ другие финансовые продукты в течение всей вашей жизни, поскольку страхование всей жизни, очевидно, может покрыть все ваши потребности, включая ипотеку, потребительские кредиты, страхование, инвестиции, сбережения на обучение и выход на пенсию.

Проблема в том, что для каждого случая страхования жизни обычно существует лучший способ решения этой финансовой проблемы. Этот пост представляет собой 38 частых мифов о страховании всей жизни, распространяемых его сторонниками.

Полное страхование жизни — не лучший способ защитить ваш доход, а срочное страхование жизни. Прежде чем выйти на пенсию, вы можете приобрести недорогое срочное страхование жизни, чтобы позаботиться о своих близких в случае вашей преждевременной смерти. 30-летний полис страхования жизни с фиксированной премией и номинальной стоимостью 1 миллион долларов, купленный на здорового 30-летнего человека, стоит 680 долларов в год. Подобный полис на всю жизнь будет стоить более чем в 10 раз дороже — 8000–10 000 долларов в год. Это деньги, которые нельзя потратить на выплаты по ипотеке или отпуск, а также инвестировать в пенсионный фонд.

Вся жизнь — не лучший способ получить постоянное пособие в случае смерти, таковым является гарантированная непрерывная универсальная жизнь. Есть несколько избранных людей, которым нужен или нужен страховой полис, который будет выплачиваться в случае их смерти, когда бы это ни наступило. Это может быть полезно для решения некоторых необычных вопросов планирования недвижимости. Однако есть лучший продукт, который обеспечивает это и который намного дешевле, чем страхование всей жизни. Это называется Гарантированное беспроигрышное универсальное страхование жизни . Он НЕ накапливает никакой денежной стоимости, а просто обеспечивает пожизненное пособие в случае смерти. Оно стоит лишь вдвое дешевле, чем страхование на всю жизнь, поэтому вы не удивитесь, узнав, что комиссия агента при этой продаже будет намного ниже.

Назовите меня циничным, но я подозреваю, что это может быть одной из причин, по которой вы никогда не слышали о гарантированной непрерывной универсальной жизни. Страхование всей жизни обеспечивает гарантированное пособие в случае смерти, которое ПРОГНОЗИРУЕТСЯ (но не гарантировано), что оно будет медленно расти, так что, если вы умрете при ожидаемой продолжительности жизни или позже, вы оставите после себя немного больше, чем первоначальное пособие в случае смерти по полису.

Полис на всю жизнь, который я недавно рассматривал, прогнозировал, что пособие в случае смерти по полису на 1 миллион долларов, купленному в 30 лет, составит 3,17 миллиона долларов в случае смерти в возрасте 83 лет. Это звучит здорово, почти как защита от инфляции в случае смерти. За исключением того, что историческая инфляция составляет около 3,1%. При ставке 3,1% 1 миллион долларов сейчас будет эквивалентен 5,04 миллиона долларов через 53 года. Вся жизненная политика будет разрушена неожиданной инфляцией, поскольку дивиденды обеспечены в первую очередь номинальными облигациями, стоимость которых будет уничтожена в условиях высокой инфляции.

Таким образом, страхование всей жизни не является ни лучшим способом предоставления гарантированного пожизненного номинального пособия в случае смерти, ни гарантированного пожизненного реального пособия в случае смерти. Так чем же это полезно? Как насчет гарантированного пособия в случае смерти, которое может увеличиться, если страховая компания захочет его увеличить? Готовы ли вы платить за это премии в два раза выше? Я так не думал.

Вся жизнь — не лучший способ инвестирования, в отличие от традиционных инвестиций. Когда вы платите страховые взносы за всю жизнь, часть денег идет на покупку страховки, часть идет на накладные расходы и прибыль страховой компании, а часть идет на комиссию продавца. Остальное затем переходит в денежную часть полиса.

Каждый год страховая компания объявляет дивиденды, и если денежная часть составляет 10 000 долларов США, а дивиденд составляет 6%, то к вашей денежной стоимости зачисляется 600 долларов США. Дивиденд применяется только к денежной стоимости, а не ко всей выплаченной премии, поэтому средняя ставка дивидендов никоим образом не связана с вашей фактической прибылью от полиса как инвестиции. Фактически, рентабельность инвестиций, как правило, будет отрицательной в течение как минимум десятилетия. Недавно я проанализировал политику для здорового 30-летнего мужчины с ожидаемой продолжительностью жизни 53 года. Гарантированная доходность от денежной стоимости составила менее 2% в год ПОСЛЕ 5 ДЕСЯТИЛЕТИЙ .

Даже если вы используете оптимистичные «прогнозируемые» значения страховой компании, вы все равно ожидаете доходность менее 5%. В действительности вы, вероятно, получите доход в размере 3–4%. Учитывая, что вам придется удерживать эти «инвестиции» в течение 5 десятилетий, это не кажется большой компенсацией. Если у вас есть десятилетия для инвестирования, гораздо разумнее пойти на больший риск со своими инвестициями и получить более высокую прибыль. Инвестиции в акции или недвижимость, вероятно, принесут доход в течение десятилетий в диапазоне 7–12%. $100 000, вложенные на 50 лет под 3% годовых, вырастут до $438 000. Если вместо этого он вырастет на 9%, вы получите 7,4 миллиона долларов, или в 17 раз больше денег. Скорость, с которой вы увеличиваете свои долгосрочные инвестиции, имеет значение, особенно в течение длительных периодов времени.

Некоторые агенты полагают, что страховые компании могут каким-то образом получить инвестиционные доходы, которые вы или я не можем найти где-либо еще, и передать эти огромные доходы владельцам своих полисов. Может быть полезно заглянуть под капот и увидеть, что на самом деле находится в портфеле страховой компании. В 2016 году активы страховых компаний были инвестированы на 67% в облигации (почти все в обычные корпоративные и казначейские облигации), 1% в привилегированные акции, 12% в обыкновенные акции, 8% в ипотечные кредиты, 1% в недвижимость, 4% в наличные, 2% в кредиты владельцам полисов и около 5% в «прочее». Благодаря революции в индексных фондах индивидуальный инвестор может купить почти все это с затратами менее 10 базисных пунктов в год. Активное управление работает для страховых компаний не лучше, чем для взаимных фондов.

Как и следовало ожидать, доходность портфеля, состоящего в основном из казначейских облигаций (в настоящее время доходность 1–2%) и корпоративных облигаций (в настоящее время доходность 3–4%), не особенно высока. Так откуда же берутся дивиденды? Часть поступает от дохода от инвестиционного портфеля, часть — от гонораров тех, кто отказался от своих полисов, а часть — от «кредитов на случай смерти», которые, по сути, представляют собой деньги, которые им не пришлось выплачивать бенефициарам, потому что умерло меньше людей, чем они планировали (т. е. вы заплатили слишком много за страховую часть полиса в первую очередь из-за государственного регулирования). Не существует волшебных инвестиций, в которые страховые компании могут инвестировать, и которые вы не могли бы сделать без компании. Каждый дополнительный слой между вами и инвестициями только увеличивает расходы и снижает прибыль.

Есть множество классов активов, которые стоит включить в диверсифицированный портфель, но вся жизнь не входит в их число. Продавцы страховых услуг обычно прибегают к этому аргументу, когда понимают, что не могут убедить вас в том, что вся жизнь сама по себе является отличным вложением средств. Они говорят, что если вы смешаете их с портфелем акций, облигаций и недвижимости, это улучшит общий портфель. Однако вы можете называть классом активов все, что захотите. Конский навоз может быть классом активов, но это не значит, что вы должны инвестировать в него. Подумайте об этом так. Если бы я сказал вам, что у меня есть класс активов со следующими характеристиками:

ты бы купил его? Конечно нет.

Вся жизнь — не лучший способ снизить расходы на инвестиционный налог, в отличие от пенсионных счетов. Многие агенты любят рекламировать налоговые льготы по страхованию всей жизни, часто сравнивая его с 401 (k) или Roth IRA. Денежная стоимость действительно растет, защищенная налогом, денежная стоимость может быть заимствована без уплаты налогов, а доходы от полиса после вашей смерти являются доходом (но не наследством) и не облагаются налогом. Поэтому некоторые сторонники всей жизни предлагают вам использовать страхование всей жизни вместо пенсионного счета, такого как 401 (k) или Roth IRA. Однако 401(k) или Roth IRA не только обеспечивает БОЛЬШУЮ экономию на налогах и позволяет вам инвестировать в более рискованные инвестиции, которые, вероятно, принесут вам более высокий доход, но вам также не придется занимать собственные деньги или платить проценты, чтобы получить такую привилегию.

Ранее я писал о трех способах, которыми 401 (k) экономит вас на налогах, и о том, чем страхование всей жизни не похоже на IRA Рота. Я также писал о том, что эффективные с точки зрения налогообложения инвестиции в налогооблагаемый инвестиционный счет не несут почти той налоговой нагрузки, которую агенты любят говорить вам. Есть ли налоговые льготы при инвестировании в страхование жизни? Да, но они сильно перепроданы.

Страховые агенты любят использовать этот метод в отношении врачей, которые могут быть параноиками в вопросах защиты активов. Однако они часто не упоминают (или, возможно, даже не знают), что законы о защите активов очень специфичны для каждого штата. Например [2022] В Алабаме только 500 долларов денежной стоимости страхования жизни защищены от кредиторов, но 100% денег в вашем 401 (k) или IRA защищены. Западная Вирджиния предоставляет защиту всего в 8000 долларов. Южная Каролина защищает 4000 долларов. Нью-Гэмпшир не обеспечивает никакой защиты. Многие штаты действительно обеспечивают 100% защиту денежной стоимости страхования всей жизни, но вам, вероятно, следует ознакомиться с конкретными законами вашего штата, прежде чем поддаться этому мифу.

Страхование жизни с денежной стоимостью имеет несколько замечательных функций планирования недвижимости, которые могут быть очень полезны. Однако подавляющему большинству людей, включая врачей, эти функции не нужны. Основное преимущество страхования жизни заключается в том, что в случае смерти вы получаете кучу денег, не облагаемых подоходным налогом. Это может помочь решить множество проблем с ликвидностью, например, владение дорогой недвижимостью или частным бизнесом. Если у вас двое детей, и вы хотите разделить свое имущество поровну, а большая часть вашего имущества — это семейная ферма, им придется либо продать ферму, разрезать ее пополам, либо заставить одного выкупить другого, чтобы разделить поровну. Однако, если бы у вас также был полис страхования жизни на ту же стоимость, что и ферма, один ребенок мог бы получить ферму, а другой - страховые выплаты. Аналогичным образом, в том счастливом случае, когда у вас очень большое имущество (более 5 миллионов долларов для одиноких людей в соответствии с федеральным налоговым кодексом, но в некоторых штатах может быть намного меньше), доходы от страхования жизни могут быть использованы для уплаты налогов на наследство. Это было бы полезно даже при наличии единственного наследника, чтобы не дать ему продать ценную собственность или бизнес по распродажной цене, чтобы оплатить налоговый счет.

Некоторым людям также нравится заключать страхование жизни в безотзывный траст, чтобы уменьшить размер своего имущества и избежать налогов на наследство. Хотя вместо этого вы можете вложить в траст простые налогооблагаемые инвестиции (и, вероятно, выиграете из-за более высокой доходности), ставки трастового налога могут быть довольно высокими, что серьезно снижает доходность неэффективных с точки зрения налогообложения инвестиций, не говоря уже о факторе хлопот. Важно отметить, что не страхование жизни экономит деньги на налогах на наследство, а тот факт, что вы отдаете свои активы перед смертью, передав их в траст.

Однако факт заключается в том, что подавляющему большинству американцев, даже врачам, в том числе врачам, имеющим «проблемы с налогом на наследство», не требуется страхование всей жизни для эффективного планирования наследства. Большинство людей умрут без какого-либо налогового бремени на наследство. Из тех, чьи поместья будут обязаны платить налоги, подавляющее большинство имеет ликвидные активы, которые можно использовать для уплаты налогов. Даже если вы хотите уменьшить размер своего имущества, чтобы избежать уплаты налогов на наследство, вы можете легко сделать это, не покупая страхование жизни. Вы и ваш супруг можете пожертвовать по 16 000 долларов США каждый [2022 — посетите нашу страницу с годовыми показателями, чтобы получить самые актуальные цифры] любому наследнику в любой год без каких-либо последствий налога на наследство/подарки. Например, если у вас было четверо детей, и у каждого было по четыре ребенка, и все 20 наследников были женаты, это 40 человек. 40 x 16 тысяч долларов x 2 =1,28 миллиона долларов в год, которые можно вывести из вашего имущества без уплаты налогов на наследство/дарение. Превышение лимита налога на наследство по такой ставке не займет много времени, и страховка не потребуется.

Некоторые агенты даже заходят так далеко, что предлагают вам использовать полис на всю жизнь для оплаты обучения в колледже ваших детей. Сможешь ли ты это сделать? Конечно. Вы просто берете политический кредит и отправляете эти деньги в университет на оплату обучения. Но вам лучше накопить на колледж, используя хороший 529 по нескольким причинам. Во-первых, вы часто получаете налоговые льготы штата, используя форму 529, которая недоступна для страхования всей жизни. Во-вторых, вам не нужно занимать деньги у своего 529, вы просто снимаете их. Никаких процентных платежей не требуется. И последнее, но не менее важное:рассмотрите временные рамки сбережений на обучение в колледже. Родители обычно откладывают деньги на обучение в колледже в течение 5–20 лет. Агрессивно инвестируя эти деньги, они могут рассчитывать на прибыль в размере 7–10%. Страхование всей жизни имеет очень низкую доходность за периоды менее 20 лет. Фактически, во многих случаях денежная прибыль от ваших «инвестиций» за всю жизнь оказывается отрицательной в течение как минимум десятилетия. Важно убедиться, что ваши деньги работают так же усердно, как и вы, и что ваши деньги находятся в отпуске в течение первого десятилетия всей жизненной политики. Сторонники страхования жизни на всю жизнь скажут, что даже если вы умрете, пособие в случае смерти все равно сможет оплатить обучение Джуниора в колледже, но гораздо дешевле покрыть этот риск с помощью срочного страхования жизни.

Страховые агенты время от времени прибегают к этому аргументу, когда указывают, что у клиента на самом деле нет никакой необходимости в постоянном пособии в случае смерти. Они признают, что клиенту на самом деле не нужна страховка на всю жизнь. Затем они пытаются продать его, считая его символом статуса или роскоши. «Конечно, тебе это не нужно, это роскошь». Роскошь – это по определению то, что вам не нужно. Я предпочитаю, чтобы предметы роскоши были чем-то, что мне действительно нравится. Поэтому, прежде чем покупать страхование всей жизни как роскошь, спросите себя:«Что мне действительно нравится?» Если у него есть страховка на всю жизнь, хорошо, купите ее. Но я готов поспорить, что большинство из нас предпочли бы такую роскошь, как хорошая машина, круиз с внуками или, возможно, пожертвование в любимую благотворительную организацию.

Вся жизнь — не лучший способ гарантировать, что у вас не закончатся деньги, а аннуитет некоторых ваших активов. Вся жизнь — не лучший способ решить проблему «второй смерти», а правильное структурирование пенсий и аннуитетов. Агенты по страхованию жизни любят придумывать сценарии выхода на пенсию, которые заставляют вас чувствовать, что вы должны иметь или, по крайней мере, хотите иметь постоянное страхование жизни, особенно для супружеской пары. Например, они будут говорить о пенсии, которая выплачивается только до тех пор, пока не умрет работающий супруг. Или они будут говорить об аннуитете какой-то части вашего имущества, исходя из жизни только одного члена пары. Затем они предложат, чтобы доходы от полиса всей жизни были использованы для покрытия расходов на проживание второго умершего супруга. Нет никаких оснований использовать политику всей жизни таким образом. Если вы хотите, чтобы ваша пенсия сохранялась до тех пор, пока вы оба не умрете, выберите этот вариант. Если вы хотите, чтобы ваша рента длилась до тех пор, пока вы оба не умрете, выберите этот вариант. Да, процент выплат будет немного ниже, но разница между выплатами меньше, чем стоимость полиса страхования всей жизни, который покроет потерю этой пенсии. Это просто не правильное решение проблемы. Обеспечивает ли страхование всей жизни некоторую гибкость при выходе на пенсию? Конечно, но цена такой гибкости слишком высока.

Вся жизнь — не лучший способ покупать дорогие вещи, надо копить на них. Есть действительно креативные продавцы страховых услуг, выступающие за такие системы, как «Банк на себя» или «Бесконечный банкинг». Основная схема такова:структурируя свой полис соответствующим образом с оплаченными дополнениями, вы получаете большую денежную стоимость своего полиса в первые годы, так что вы выходите на уровень безубыточности через 3-4 года, а не через 8-15 лет. Вы также покупаете политику «непрямого признания». Это означает, что когда вы берете кредит по полису, страховая компания продолжает выплачивать дивиденды на сумму, которая была у вас до того, как вы его взяли взаймы, поэтому дивиденды по полису по существу компенсируют процентные платежи, причитающиеся по кредиту. Теперь вместо того, чтобы идти на свой сберегательный счет или в банк, чтобы занять деньги, когда вам нужна машина, холодильник или инвестиционная недвижимость, вы берете взаймы всю свою жизнь практически бесплатно. Кроме того, денежная стоимость полиса, который вы не берете в долг, будет расти быстрее, чем деньги в сберегательной кассе.

Так в чем проблема? Проблема в том, что вам придется покупать полис на всю жизнь, который вам не нужен. Вы можете выйти на уровень безубыточности раньше, чем при традиционной политике, но все еще есть несколько лет отрицательной доходности и в долгосрочной перспективе такая же низкая доходность. Что лучше — зарабатывать 4–5% в год через 5 лет или зарабатывать 1% в год, начиная с первого года? Что ж, в течение первых 6 или 7 лет вам лучше иметь сберегательный счет под 1% в год. Кроме того, если процентные ставки поднимутся с исторического минимума, вы все равно будете привязаны к этой системе на всю оставшуюся жизнь. Не так давно я мог получить более 5% от фонда денежного рынка. Также кажется, что очень легко профинансировать покупку автомобиля в автосалоне по чрезвычайно низким процентным ставкам. 0% или 1% не являются редкостью. Вам лучше брать у них кредит под 1%, чем у вашего полиса под 5%. Аналогичная проблема с бытовой техникой и ипотекой. Вы прилагаете все усилия, чтобы занять деньги у самого себя, а затем понимаете, что дешевле взять кредит у кого-то другого. Наконец, если вам не нужно совершать покупку в течение 5 или 10 лет, у вас есть время инвестировать во что-то, что может принести гораздо более высокую прибыль, чем полис на всю жизнь. Обманывают ли тех, кто рассчитывает на себя? Не обязательно, но они, как правило, переоценивают преимущества своей схемы. Его сторонниками являются в первую очередь страховые агенты, стремящиеся увеличить продажи с помощью креативного маркетинга. Экономия – это лучший способ совершать крупные покупки, чем покупать полис на всю жизнь.

Сторонники страхования на всю жизнь, особенно те, кто выступает за использование вашего полиса в качестве банка, любят отмечать, что множество очень богатых людей и множество предприятий (включая банки) на самом деле покупают страхование на всю жизнь. Это правда, но для обычного человека это не имеет значения. Крупный бизнес не имеет доступа к вариантам пенсионного счета, позволяющим сэкономить на налогах, которые есть у человека среднего класса. Сверхбогатые люди уже достигли максимума. Когда у вас гораздо больше денег, чем вам когда-либо понадобится, прибыль от ваших денег не имеет такого большого значения. Билл Гейтс может позволить себе инвестировать во что-то, что приносит доход в размере 2–5%, потому что ему не нужны деньги для тяжелой работы. Это просто неверно для подавляющего большинства людей среднего и высшего класса, включая врачей. Как обсуждалось выше, сверхбогатые люди также больше используют ограниченные льготы по планированию недвижимости и преимущества по защите активов постоянного страхования жизни. Короче говоря, низкая доходность, присущая всей жизни, для них гораздо меньшая проблема, чем для вас.

Продавцы всей жизни любят подчеркивать, что вся жизнь обходится намного дешевле, если вы покупаете ее в молодом возрасте. Хотя это правда, что страховые взносы ниже, если вы покупаете полис в 25 лет, чем если вы покупаете его в 55 лет, если принять во внимание временную стоимость денег и тот факт, что вы будете платить премии в течение трех дополнительных десятилетий, это не лучшая инвестиция в молодом возрасте, чем в более старшем возрасте. Актуарии — очень умные люди, и для риска, который относительно легко смоделировать, например смерти, они могут достаточно эффективно оценить страховку.

Помимо более низких страховых взносов, есть еще две причины, по которым лучше покупать его, когда вы молоды. Во-первых, эта комиссия распределяется на большее количество лет, поэтому она меньше влияет на вашу общую прибыль. Но альтернатива вообще не платить комиссию гораздо более привлекательна. Во-вторых, вполне возможно, что в более позднем возрасте вы либо ухудшите свое здоровье, либо займетесь каким-нибудь опасным видом спорта. Это один из серьезных недостатков использования страхования жизни в качестве инвестиции:не каждый может его использовать. Либо они вообще не имеют на это права, либо цена страховки настолько высока, что прибыль от инвестиций оказывается даже ниже, чем была бы в противном случае. Я не вижу в этом причины покупать его, когда ты молод, я вижу в этом причину не покупать его вообще. Можете ли вы представить, если бы компания Vanguard послала к вам на дом фельдшера, чтобы взять кровь, прежде чем позволить вам купить их фонд S&P 500?

Страхование всей жизни — не лучший способ защитить ваш пенсионный доход от инвалидности, а страхование по инвалидности. Понимая, что страховые взносы по страхованию всей жизни действительно дороги и их будет сложно произвести в случае инвалидности, страховые компании начали предлагать программу, которая отказывается от страховых взносов в случае вашей инвалидности. Иногда кажется, что вам даже не придется доплачивать за это преимущество. Те, кто попадается на эту тактику, теряют пару очков. Во-первых, гарантии не бесплатны. Каждая гарантия стоит вам денег в виде более низкой прибыли, независимо от того, взимает ли страховая компания дополнительную плату за гарантию или «включает ее в полис», чтобы она была скрыта.

Во-вторых, страхование по инвалидности является сложным, и определение инвалидности очень важно. Большинство врачей, которые хотят получить страховку по инвалидности, тратят много денег на получение действительно хорошего полиса с широким определением инвалидности, включая страхование «собственной профессии», потому что они хотят быть уверены, что компании придется платить в случае их инвалидности. Пассажиры, продающие полисы на всю жизнь, не так полны, и у них гораздо меньше шансов получить оплату во многих серых зонах, в которые часто попадают инвалиды. Вам почти наверняка будет лучше купить более крупный полис по инвалидности, чем пожизненный отказ от премиум-райдера. Ваша страховка по инвалидности также может предлагать пенсионную защиту. Хотя и здесь есть проблемы (в первую очередь, в способе выплаты пособия), это лучше, чем пытаться получить страховку по инвалидности по полису на всю жизнь.

Если вы, как и я, планируете досрочный выход на пенсию, вы, возможно, поймете, что вам все равно не нужна страховка по инвалидности для защиты пенсионных взносов, по крайней мере, после нескольких лет крупных сбережений. Подумайте о том, чтобы иметь портфель в 750 тысяч долларов в возрасте 40 лет. Вы полагаете, что вам нужно 2 миллиона долларов в сегодняшних долларах для выхода на пенсию. Вы планируете накопить значительные средства, чтобы достичь этого в 50 лет и выйти на пенсию. Каков запасной план, если вы станете инвалидом и не сможете накопить все эти деньги? Ваша страховка по инвалидности выплачивается не только до 50 лет. Она выплачивается до 65 лет. Таким образом, вам не нужен ваш портфель, чтобы покрыть эти 15 лет. Вы также можете начать получать выплаты социального обеспечения к тому времени, когда закончатся выплаты по инвалидности. Поскольку вам не нужно трогать свое портфолио, оно может продолжать расти. Если после инфляции он вырастет на 5%, то к тому времени, когда вам исполнится 65 лет, он будет стоить более 2,5 миллионов долларов в сегодняшних долларах. Не покупайте страховку, которая вам не нужна. Но даже до того, как у вас появится какой-либо портфель, лучший способ защитить свои пенсионные сбережения — это купить БОЛЬШЕ страховки по инвалидности, а не пытаться получить ее от полиса на всю жизнь. Даже если бы вы могли использовать дополнительное страхование для обеспечения своего пенсионного портфеля, вам необходимо иметь возможность вложить его в инвестиции с высокой доходностью, которую вряд ли обеспечит вся жизнь. Агрессивно инвестируемый налогооблагаемый счет вполне подойдет, поскольку ваш основной доход в случае инвалидности и пособия по страхованию по инвалидности не облагаются налогом.

Поскольку агент получает новую комиссию каждый раз, когда продает новый полис, даже если он заменяет старый от той же компании, у него возникает серьезный конфликт интересов при предоставлении вам рекомендаций. В этом блоге я общаюсь со многими страховыми агентами, и ни один из них не согласен с другими в том, что такое «правильно структурированный» полис на всю жизнь. Это означает, что если вы пойдете ко второму агенту, он почти наверняка скажет вам, что есть лучший способ сделать это. Однако для того, чтобы иметь смысл менять одну политику на другую, первоначальная политика должна быть абсолютно ужасной, особенно спустя пару десятилетий. Причина этого в том, что низкие доходы от страхования жизни сконцентрированы в первые годы. Недавно я взглянул на политику. Это было оформлено как инвестиция с оплаченными дополнениями в течение первых 25 лет. Это была лучшая попытка агента максимизировать прибыль от полиса. Вот как выглядела годовая прибыль:

Гарантировано Прогнозируемое Первые 10 лет-1,84%0,98%Следующие 15 лет2,55%5,47%Следующие 25 лет1,99%5,13%Это показывает, что низкие доходы в значительной степени сконцентрированы в первые годы. При использовании этой конкретной политики прибыль фактически снижается через 25 лет, потому что именно тогда вы перестанете вносить оплаченные прибавки. При более традиционной политике третий ряд будет немного выше второго. Но мораль этой истории в том, что сначала вам следует купить «правильную политику», и даже дрянная политика, которой более 10 лет, будет лучше, чем совершенно новая, лучшая политика. Это также причина того, что может быть хорошей идеей сохранить старый полис на всю жизнь, даже если его покупка изначально была ошибкой. Также примечательно то, насколько малый риск на самом деле принимает на себя страховая компания, поскольку она даже не гарантирует, что ваша денежная стоимость будет соответствовать инфляции.

Вся жизнь — не единственный способ передать деньги наследникам без уплаты подоходного налога в случае вашей смерти. На самом деле, это даже не лучший путь, ИРА Рота. Когда вы умрете, ваши наследники получат страховое пособие в случае смерти, не облагаемое подоходным налогом. Агенты часто забывают упомянуть, что почти все, что ваши наследники получат от вас после вашей смерти, не облагается подоходным налогом. Благодаря увеличению базиса в момент смерти все, что находится за пределами пенсионного счета, включая мебель, автомобили, акции, наличные, взаимные фонды и недвижимость, переоценивается в день вашей смерти. Поскольку база теперь такая же, как и стоимость, налог на прирост капитала не подлежит уплате. Унаследовать пенсионный счет может быть еще лучше, особенно счет Рота, по которому уже уплачены налоги. You can take all the money out the same year you inherit it and not pay any taxes at all. Or, you can “stretch it”, taking withdrawals gradually over decades until you die. Meanwhile, it continues to grow tax-free. You can stretch an inherited tax-deferred account too, but you do have to pay taxes on any money withdrawn from the account.

People invest in whole life insurance because they like guarantees. The insurance company guarantees that you'll get a certain rate of growth on your investment and it guarantees a death benefit. The guarantees, however, aren't worth nearly as much as people often assume. For instance, the guaranteed scale of any whole life insurance policy guarantees that your money will grow slower than the historical rate of inflation, despite sticking with it for half a century. Before deciding to trust a single company with your life savings, you might want to consider what happens if it goes out of business. There are state insurance guarantee associations that will cover the cash value and death benefit of your policy, but how much will they really cover? You might be surprised how little it is. In my state, only $500K in death benefit and $200K in cash value is covered, NO MATTER HOW MANY POLICIES YOU OWN. Your state is probably similar. No wonder agents are always talking about the long-term viability of their insurance company. It really does matter! Now I don't think the risk of any given insurance company going out of business in any given year is very high, nor do I think a typical purchaser is likely to end up with exactly the guaranteed growth rate. But before buying, you should realize that investing in whole life insurance isn't the risk free proposition agents like to present it as.

This one is pretty easy to see through, but you still see agents using it frequently. Since everyone “knows” that it is better to own a home than rent one, the agent says something like “You wouldn't rent your home for the rest of your life would you? So why would you rent your life insurance?” Basically, the agent is referring to the fact that if you use term insurance after age 60 or so, it becomes more and more expensive each year, just like renting a home. But unlike a home, you don't need life insurance after you become financially independent. When you only need a home for a year or two or three, it is a better idea to rent than to buy. When you only need life insurance for a decade or two or three, it is also a better idea to “rent” than to buy. The opportunity cost of “ownership” is simply too high.

This is a frequent one heard from the Bank on Yourself/Infinite Banking crowd. An underpinning of this school of thought is that the greedy banks are taking over the world so you should only do your financial work through the trustworthy insurance companies. To be honest, I don't have massive distrust for either one of these industries. Both industries have mutually-owned options (mutual life insurance companies and credit unions) where, like Vanguard, the customers own the company. The agents like to point out that banks actually own whole life insurance as part of their “Tier One Capital,” the money used to determine if the bank is adequately capitalized or not. This is somehow to make you fear that the banks know something you don't, like the financial world is about to implode and any of those using banks instead of insurance companies for their financial needs are going to go broke. Tier One Capital is a measure of a bank's financial strength. Banks use less than 25% of their Tier One Capital to buy single premium whole or universal life insurance on a group of employees. The bank owns the policy and is the beneficiary. When the employee keels over, the bank gets the cash. The bank is buying the policy primarily for the death benefit, not because the return is particularly high.

Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock(aside from that of the bank, which makes up most of Tier One Capital) and REITs in its Tier One Capital. When you are stuck choosing between low-risk/low-return investments, then you can understand why a bank might consider something like cash value life insurance with part of that money. However, individual physician investors investing for retirement have fewer restrictions on their investment options for their retirement. Most of them have significant need for their retirement money to grow. The returns available with cash value life insurance generally are not high enough for them to reach their goals. Even so, consider what a bank does with most of its Tier One Capital—it buys the only stock it can, it's own. If whole life insurance was so awesome, you'd think the bank would use all of its Tier One reserves to buy it. In short, doctors aren't banks, so doing what banks do isn't necessarily smart. Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock.

Agents, particularly of the Bank on Yourself type, love to point out that the golden parachutes for many highly-paid CEOs include cash value life insurance policies. However, just as the financial situation of a bank is dissimilar from that of a physician, so is the financial situation of a CEO making $10 Million a year different from that of a physician. When you're making a gazillion dollars a year, rate of return on your money becomes much less important and thus the benefits of whole life (asset protection, tax, estate planning, etc.) become relatively more important. It isn't that returns on whole life magically get better. Again, if you are in a position that you only need your long-term money to grow at 3%-5% nominal per year, then feel free to invest in whole life insurance. Most of us, however, need higher growth. Remember that a doctor making $200,000 per year and a CEO making $10 Million per year are in very different financial circumstances and what works fine for one will not necessarily work well for the other.

This myth again preys on the fears of a global economic meltdown. In 1933 there were two holidays. The first was a “Banking Holiday” in which the banks were closed for 10 days as sweeping regulatory changes took place. The second was an “Insurance Holiday” in which for a period of nearly six months you could neither surrender your cash value life insurance policies for cash, nor borrow against them. Aside from this holiday, 14% (63 companies) of life insurance companies actually DID fail during The Great Depression. In fact, if they would have actually marked to market the bonds and mortgages they held, they would have ALL been insolvent. Reforms were put in place during The Great Depression that fixed many of the problems leading to bank failures and the banking holiday. However, these reforms were never put in place for insurance companies.

This one usually goes like this. “If you can buy a bond yielding 5% and are in a 45% marginal tax bracket, the after-tax yield on that is just 2.75%. A whole life policy with a “tax-free” internal rate of return of 5% is better.” This is an apples to oranges comparison. What is the 1 year return on that whole life policy? 2.75% sounds a whole lot better to me than a -50%. Even at 10-20 years, the bond is still way ahead.

I wrote about a physician who was pleased with his 7% return on his whole life policy bought in 1983 (don't expect to see that again any time soon). Except that he could have bought a 30-year treasury that year yielding 10.5%. 10 years later, as his whole life policy is breaking even and interest rates have dropped, the bond purchaser has not only already more than doubled his money just from the coupon payments, but the capital gains on that bond added another 50% to his return. That investor would have done even better purchasing equities in 1983, the start of an 18 year bull market. A bond, which can be sold any day the market is open, simply cannot be compared in any fair manner to an insurance policy which must be held for life to have any decent kind of return. Besides, most physician investors can hold taxable bonds inside retirement accounts instead of a taxable account anyway. That retirement account not only provides for tax-protected growth like a whole life policy, but also a tax-rate arbitrage between your marginal rate at contribution and your effective rate at withdrawal, further boosting returns.

Even if your only choice is between buying bonds in a taxable account and buying whole life insurance, keep in mind that even at today's low interest rates you can still buy Vanguard's Long-Term Tax Exempt Muni Fund yielding 3.17% [2014] . The guaranteed return on whole life insurance cash value, held until your life expectancy, is about 2% and the projected return is only ~5%. Realistically, you should probably expect a return of 3%-4% over the long term on that policy. Of course, if you actually wish to cash out of that policy instead of borrowing from it (and paying interest for the right to borrow your own money), the earnings are just as taxable as any taxable bond fund. And if you want your money in a mere 10-20 years, you're going to come out way behind with the life insurance.

Now, if you really understand how whole life insurance works and you think its unique features outweigh its significant downsides, then feel free to run out and purchase as much as you like. It truly does not bother me. I do not make any money if you buy whole life, nor if you decide to buy something else. However, if you are like most, once you understand it, you won't buy it and in fact, if you already have, you'll probably be looking for the best way to get out of whole life insurance. Не расстраивайтесь. 80% of those who purchase these policies surrender them prior to death, 36% within just five years. You've got to ask yourself why so many people who were apparently intending to hold this product for the next 40 or 50 years suddenly changed their mind. I'm sure it has nothing to do with it being inappropriately sold to the financially unsophisticated by insurance agents facing a terrible financial conflict of interest with their clients. Whole life insurance is a product made to be sold, not bought. It is a solution looking for a problem that exists for very few, if it exists at all.

This is one is merely misleading. The statement as it stands is true. The Free Application for Federal Student Aid (FAFSA) does NOT consider whole life insurance cash value as an asset of the student or the parents. The problem is, for the typical reader of this blog, that it doesn't matter. Your income alone will keep your child from qualifying for any need-based college financial aid. So if you buy a whole life policy for this reason, you're likely to be disappointed.

Another misleading argument. I'm always surprised to see people fall for this line, but they do. Do you complain when you don't get to use your car insurance for any given six month period? How about when your house doesn't burn down? Or you don't get cancer and get to use your health insurance? Then why in the world would you complain that your term life insurance expires and you're still alive. Term life insurance is pure insurance. If you die, it pays. If you live, it doesn't. As a general rule, since on average insurance must cost more than it pays out (since insurance companies have both expenses and profits), you should insure against financial catastrophes. When it comes to death, the financial catastrophe is dying during your earning years, before you become financially independent. So that's the only time period you need to insure against. Some people only fall halfway for this argument, and buy return of premium term life insurance. The same principle applies, of course. You don't walk away empty-handed when your term life policy expires. You had insurance for the entire term, which is exactly what you needed.

This outright lie comes from the true believers. They argue that whole life insurance is safe, liquid, tax-advantaged, creditor-proof, and offers a competitive return. These half-truths all add up to one big lie. Let's take them one at a time:

Safe from the cash value going down, perhaps, but not safe from losing money. A huge percentage of whole life insurance purchasers lose money because they cancel the policy at some point in the first 5-15 years before they break even on their “investment.”

I guess it's more liquid than owning a website or a rental property, but it pales in comparison to the liquidity available in a savings account or a mutual fund that can be liquidated any day the market is open. Even inside retirement accounts, there is absolute liquidity after age 59 1/2, and fair liquidity even prior to that date. Most of the time with whole life insurance you don't even get your money, you just have the right to borrow against it at pre-set terms. You can get that with a HELOC.

Few understand just how minor the tax advantages of whole life insurance are. There is no up-front deduction like a 401(k). Unlike a real investment, there are no capital gains rates if you surrender a policy with a gain and you cannot deduct the loss if you surrender it with a loss (the usual case). You don't get to use depreciation to reduce the tax burden of your income like with real estate. Instead of being able to withdraw the money tax-free like with a Roth IRA, you can only borrow against the policy, and that's tax-free but not interest-free, just like borrowing against your house, car, or mutual fund portfolio. Sure, you don't pay taxes on the “dividends,” but that's because they're actually a return of premium (i.e., you paid too much for the insurance). The only real tax break associated with life insurance is that the death benefit is tax-free. But that isn't any different from any other investment, where you get the step-up in basis at death. In addition, whole life can't be stretched like an IRA. The tax benefits, such as they are, are limited to a single generation.

Too few docs understand just how low the risk of needing this protection actually is. I calculate my risk of being successfully sued for an amount above policy limits at 1 in 10,000 per year. Maybe half that now that I'm practicing half-time. So should I be so unlucky as to be that one person, I would declare bankruptcy and be left only with protected assets. In my state, that's my retirement accounts, my spouse's assets, $40,000 in home equity, and whole life insurance cash value. Your state may or may not protect whole life insurance cash value. Please actually check if you are so paranoid to actually buy whole life insurance for this reason.

Ты шутишь? Competitive with what? Whole life insurance generally has a negative return for 5-15 years (sometimes more than 30 for really terrible policies). Even a good policy held for 5+ decades only guarantees a 2% return and projects a 5% return.

If I were going to draw up the perfect investment, it would definitely avoid the following characteristics of whole life insurance

It only qualifies as an “okay” investment in certain very limited situations. It's not even close to a perfect one.

This is one of my favorites to see in any sort of discussion with an insurance agent about the merits of whole life insurance. It usually comes when I point out that my problem with whole life insurance isn't so much the product as the way in which it is sold. Obviously, many of them take that quite personally since they've dedicated their life and career to selling this product inappropriately. So they point out that there are bad doctors or that insurance agents are just people trying to make a living. I don't have a problem with the sales profession. I don't even have a problem with people earning commissions for selling stuff. Cindy gets paid on commission to sell ads right here at The White Coat Investor. But if you seek advice from Cindy about whether buying an ad at The White Coat Investor is a good idea for you, you're a fool. Insurance agents are just people and people respond to incentives. An insurance agent has a huge incentive to sell you a whole life policy. The commission on a policy is 50%-110% of the first year's premium. Now you know why he's trying so hard to sell you a big fat doctor policy.

This was a new one to me. I thought I had heard every possible argument for buying a whole life policy until someone whipped this one out. How much trouble is it for you to deal with a 1099? It takes me about 30 seconds using Turbotax. Certainly not a reason to favor one investment over another. Remember not to let the tax tail wag the investment dog. Your goal isn't to minimize your taxes or maximize your tax-free income. It's to have the most money AFTER paying the taxes due.

Sometimes agents start with this argument, but frequently this is where they end, with ad hominem attacks. Sometimes it's phrased like one of these:

So, exactly how does being an ER doctor qualify you to give financial and insurance related advice?

Do everyone a favor and stick to studying medicine.

You’re young, a doctor and absolutely sure that you know everything.

Obviously, medicine has lots of problems and doctors don't know everything, but if the agent's best argument for whole life insurance is an ad hominem attack, that's a good sign that you should have stood up and walked out a long time ago.

This is the wrong question to be asking, but the answer to it is still no. Just because it is the only option presented to you by an insurance agent, doesn't mean it is the only option. Other options for retirement savings include defined benefit/cash balance plans, an individual 401(k) for self-employment income, a spousal Roth IRA, your spouse's employer-provided accounts, and Health Savings Accounts (HSAs). In some ways doing Roth conversions and paying off debt is also tax-sheltered. But most importantly, there is no limit on investing in a non-qualified mutual fund account (where long-term gains and qualified dividends are somewhat sheltered from taxes) or in real estate (where income is sheltered by depreciation and capital gains can be deferred indefinitely by exchanging).

Obviously investing in whole life insurance compares better to investing in a taxable account than to a retirement account (where there is no comparison from a tax, investing, or in most states an asset protection standpoint). But the real problem with this argument is that it is focused entirely on the idea that any tax-advantaged investment is always better than any fully taxable investment. That simply isn't true. It also mixes up the idea of an investment and an account, two things that financially naïve doctors sometimes have a hard time telling apart. (Think of the accounts as different types of luggage and the investments as different types of clothing.) The real question to ask yourself when you hear this argument is “Where should I invest after maxing out my available retirement accounts?” The answer is a taxable, non-qualified account. Now you're left with the question of what long-term investment to invest in—tax-efficient mutual funds, real estate, or whole life insurance? It's pretty hard to really compare the merits of those three investments and end up choosing whole life insurance given its limitations and terrible returns previously discussed.

The idea behind this argument is a rebuttal to the argument discussed in Myth #8. In summary, that argument is that you need whole life to avoid estate taxes, which is silly given the vast majority of doctors won't owe any federal estate taxes. The next step is for the agent to argue “Well, the estate tax exemption might be decreased.” Well, I suppose that's true. Congress can change any law they want any time they want. But buying insurance or investing based on what could happen seems foolhardy. I mean, it is probably just as likely that the estate tax is eliminated as the exemption reduced. It seems to me the best way to plan for the future is to project current law forward, since most laws aren't going to be significantly changed. If they are, you can make changes at that point. At any rate, it isn't like whole life insurance is some magic panacea to eliminate estate taxes. The only reason whole life insurance reduces your estate taxes is by making sure you have less money due to its low returns! The thing that reduces the size of your estate is the irrevocable trust you put the insurance into, and you don't even have to put insurance into it if you don't want to.

This one was particularly fun to debunk. Apparently, the idea here is to not pay for your own nursing home care somehow by purchasing whole life insurance instead of mutual funds. I'm not sure exactly how those envisioning this process think it will go. Maybe they think the nursing home doesn't ask for money until after you die or something, which is, of course, completely silly. But I think what they're referring to is the ability to spend down your assets to Medicaid levels, get Medicaid to pay for the nursing home, and still be able to leave a huge inheritance to your heirs because Medicaid somehow doesn't look at the value of your whole life insurance.

The whole process of Medicaid planning is a little distasteful to me to be honest. The idea is to hide someone's assets from the state so that the heirs can have them, foisting the cost of caring for the owner of those assets on to the public. But even assuming that you have no ethical problem with doing this, it's unlikely to work very well. Medicaid is state law, so it varies by state, but in Utah, a person can have up to $2,000 in countable assets and still qualify for Medicaid. Above that level, no Medicaid until you spend down to that level. If there is a spouse, the spouse can keep 100% of assets up to $24,720 and 50% of assets up to $123,600. Above that, Medicaid won't pay for the nursing home. Non-countable assets in Utah include:

So I guess if you want to hide money from Medicaid in Utah, then you could go buy a $1,000 whole life policy. Most states have similar policies regarding cash value life insurance. Even if there were a state with a higher limit than Utah, this seems silly for someone who should spend her entire retirement as a multimillionaire to be making plans to spend down to Medicaid levels for nursing home care. A far better plan to stiff your fellow Utah taxpayer (assuming you have a spouse who doesn't need care) is to upgrade your house and your car.

This statement has been made without explanation, but the idea isn't that complicated (nor misunderstood by WCI). You can borrow against the cash value in your whole life policy and use that money for whatever you want. You can spend it or you can invest it. Lots of whole life fans use fun phrases like “velocity of money” to describe buying a whole life policy, borrowing the money out, and investing it in something else. The really talented salesmen get you to invest it (along with any home equity they can get you to borrow out) in yet another insurance product.

Is there a cost to not maximally leveraging your life in this manner? Sure, anytime you can borrow at a lower rate and earn at a higher rate you'll come out ahead. But leverage works both ways, and the risk is not insignificant. What is not often mentioned by those advocating doing this is the opportunity cost of plunking money into a low return life insurance policy and buying unneeded death benefit instead of a higher returning investment. For instance, consider two options. You can invest $10K a year into an investment that returns 10% per year or you can buy a whole life policy that won't break even for 10 years. After 10 years, the first investment is worth $175K and the whole life policy only has a cash value of $100K. That's a $75K opportunity cost that apparently the “insurance agent doesn't understand.”

With a properly structured policy, you can break even in perhaps five years (maximizing the use of Paid-Up Additions), and using the combination of wash loans (interest rate to borrow against the policy =dividend rate of the policy) and a non-direct recognition policy, this idea becomes “not terrible.” You still have the opportunity cost of the first few years in the policy, but that is balanced out by a higher return on your cash in later years. I have discussed “Bank on Yourself” or “Infinite Banking” previously in detail if you are interested. It's not an insane use of whole life insurance, but it isn't for me. If you really understand how it works (it's going to take working through a lot of hype to do so) and want to do it, go for it.

In recent years, insurance companies are adding on a Long Term Care rider to whole life insurance policies (and universal life policies and annuities) and agents are using the fear of expensive long term care to sell them. I find this appalling. Not only are you mixing insurance and investing, but you're now combining two different types of insurance policies with investing. Given the track record of insurance companies with long term care, I think most of my readers should strive to get a place where they can self-insure the risk of long term care, but even if they cannot, I'd prefer a simpler long term care policy on its own than mixing it with an otherwise unnecessary and expensive insurance policy.

The benefit of buying this as a rider of a whole life policy is that the premiums of the policy are guaranteed—you don't have the risk of the insurer upping the premiums like you do with a long term care policy or upping the cost of the underlying insurance like you do with a universal life policy. Those guarantees are worth something.

Remember we're not talking about just an accelerated death benefit. This is just another way of self-insuring long-term care, but with a lower return on the investments used to pay for it. You're really buying two policies combined into one. But there's no free lunch here. You're either paying more for the combined policy, or you're getting less of something, usually death benefit. Most likely, you're also paying for a life insurance policy you don't need or wouldn't otherwise buy. That death benefit isn't free. The reason life insurance companies stopped selling long term care insurance and started selling these hybrid policies is that their actuaries were convinced they are more likely to make money that way. That profit has to come from you, there is no other possible source.

If you do decide you wish to purchase some sort of long term care insurance policy, it is entirely possible that a hybrid product is right for you, but just like health and disability insurance, the devil is in the details. Read the fine print and be sure you know what guarantees the insurance company is actually providing. Know about what is covered, what isn't covered, and whether benefits are indexed to inflation or capped. Or better yet, live like a resident for 2-5 years out of residency so you'll be rich enough to self-insure this risk and never have to make this decision.

This argument is simply bizarre, but used by agents once the prospective buyer has refused to buy the massive policy they were offered at first. A small commission is better than no commission, I guess. Of course, you shouldn't put all your money into whole life insurance, that's a straw man argument. Also, if buying a policy is a bad idea, you're going to be better off if you buy a small one than a big one. But that's hardly a reason to buy a policy in the first place. Like any asset class, if it isn't a good idea to put a significant chunk of your portfolio into it, it probably isn't a good idea to put any of your money into it.

This argument is used when I point out that literally hundreds or even thousands of my readers have been sold clearly inappropriate insurance policies. The problem is there are two options to explain this phenomenon. The first is that these agents are unethical. The second is that they're incompetent. Given the statistic that 80% of policies are surrendered prior to death and 76% of the docs I've surveyed regret their purchase, this is hardly just a “Few Bad Eggs” doing this. It's an industry-wide problem.

This one is used to sell insurance to people that don't even have a need for insurance. The idea is to prey upon their fear of the combined risk of needing insurance AND not being able to purchase it. One example would be a 25-year-old single doc with no kids. No life insurance need here. “But what if you get diabetes before you get married and have kids? You should buy the policy now.” Uhhhh . . .no.

First, you may never have dependents.

Second, if you do need it, you'll probably be able to buy it at that time at a reasonable price.

Third, if you do become less insurable, you will still likely have options for some insurance through an employer or other groups.

Fourth, even if you become uninsurable through anyone, the risks must be multiplied. For example, let's say there's a 5% risk of you becoming uninsurable before you have a real insurance need. And the risk of you dying before reaching financial independence is 5%. To get your true risk of a financial catastrophe, you must multiple those risks. 5% x 5% =0.25%. That is a 1 in 400 chance. Life is risky. You can't eliminate every possibility of something bad happening to you and even if you could, that wouldn't be a wise use of your money. Wait to buy insurance until you have a need for that insurance.

This argument is often even extended to children. If you're buying life insurance from the same company that sells you baby food, you're probably doing something wrong. Now, if you could buy a lot of future insurability for that kid very, very cheaply, that might be something to consider. Unfortunately, you can't really do that for several reasons:

First, you have to actually buy unneeded insurance. That newborn likely won't have any need at all for life insurance for 25-30 years.

Second, you're not pre-buying the policy that kid will need. You can't buy the right to buy a 30-year level term policy at age 30. You have to buy a whole life insurance policy. Which means you're also paying for insurance that will be unnecessary on the far end of life too, after the kid has become financially independent.

Third, you generally can't buy enough insurance, or even enough future insurability, to actually meet any sort of realistic life insurance need. Most of these infant policies are only $10K or so. That's basically a burial policy, and as sad as it would be to bury your kid, it's not a financial risk my readers should need to insure against. (I've even heard the argument that you should buy the policy so you can take a few months off work because you'll be too distraught to work, but that's what an emergency fund is for.) Even if you find a policy that allows you to purchase future insurability for a larger policy, let's say $500K, that's not going to mean much in 30 years when the life insurance need actually shows up for the first time, much less in 50 years when the kid is actually reasonably likely to die. At 3% inflation, $500K today will only be worth $200K in 30 years and $109K in 50 years. Better than nothing, but you went to all this effort and expense to preserve insurability and your kid still ended up with inadequate life insurance coverage.

I had this one pitched to me by a doc turned financial advisor of all people. The argument was that you could buy whole life with pre-tax dollars and then if you wanted to pull the policy out of the defined benefit plan you could do so. He felt this was an “advanced technique” for “high net worth folks.” I was flabbergasted. It was such a stupid idea I couldn't believe it. A defined benefit/cash balance plan already provides tax protected growth and asset protection, two reasons frequently cited to buy whole life insurance. You're now paying twice for those benefits. To make matters worse, should you die while this policy is in the defined benefit plan, part of the death benefit becomes taxable, negating another usual advantage of life insurance—a completely tax-free death benefit. But the main reason why this is such a stupid idea is when it comes time to close the defined benefit plan, which is usually done every 5-10 years or so in order to roll it into an IRA. At that point, you have to do one of two things.

First, you can surrender the policy and move the cash surrender value into the IRA. But what is the investment return on the first 5-10 years of a whole life policy? You break even if you're lucky. Not exactly a great investment for that time period, especially compared to a typical conservative mix of stocks and bonds.

Second, you can purchase the policy from the plan. Of course, you have to do that with AFTER-TAX dollars. So while you initially bought it with the pre-tax dollars in the plan, eventually you're going to have to cough up after-tax dollars for the policy. And then what are you left with? A whole life policy you probably neither want nor need and perhaps even with associated premiums you have to make each year. Some deal!

This myth showed up in a comment on a post on this blog. I thought it was particularly creative, especially with the way it was combined with Myth #8 (You Need Whole Life to Help For Estate Planning) and Myth #25 (Term Life Expires Without Paying Anything):

More money is passed through life insurance than any other way. I’ve seen too many people out live term which is throwing money away and need life insurance and are at that time in life uninsurable. Life is really used well in estate and trust planning.

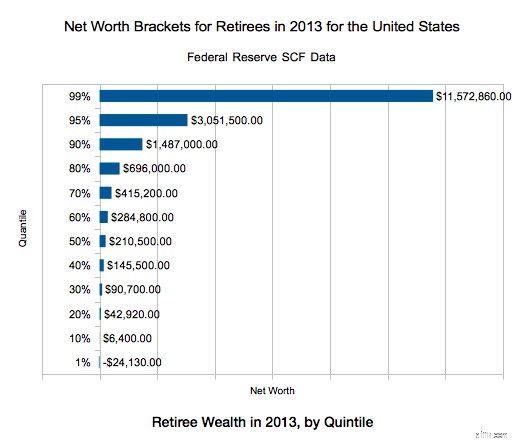

Surprisingly, this was the first time I had heard this argument. Being financially literate, of course I was able to immediately debunk it, but I suppose somebody might fall for it. There are two problems with this statement. First, it may not even be true. I looked and looked and looked for a study that showed what assets are actually inherited, without finding anything that actually quantified it. So if there is a study that actually says this, I suspect it is paid for by a life insurance company. Maybe it's true, maybe it's not, but I suspect it isn't given how few people have life insurance in force at their death. I suspect more money is left behind in houses than anything else. I mean, look at the net worth of people by age. Among retirees, the 50th percentile for net worth is $210K. That's got to be mostly house. The 80th percentile is $696K. That's about the average price of a house in my upper middle class neighborhood in a flyover state.

That jives with the average estate left behind at death:

It seems very unlikely that the main inheritance most people receive is the proceeds of a life insurance policy given those numbers. How many retirees even carry life insurance? According to this, about 65% of those 65+. But 47% of those own less than $100K of life insurance. It is a well known statistic that fewer than 1% of term life insurance policies pay out. It isn't that the insurance companies aren't good for the money, it's just that people out live the term. A lesser known statistic is that 80%-90% of whole life insurance policies don't pay out either. They're surrendered prior to death, often at a loss since 1/3 of policies are surrendered in the first 5 years and over half in the first 10 years.

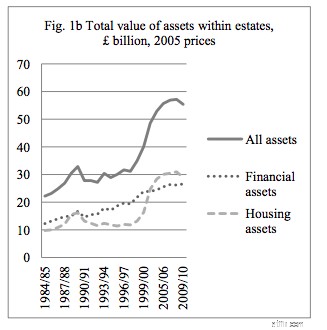

I did manage to find some UK data, however, which suggests my hunch (that people inherit more in real estate than life insurance proceeds) is correct.

As you can see, more than half of inherited assets are housing assets, so clearly more assets cannot be passed as life insurance than anything else.

Perhaps the agent wasn't referring to the median inheritance though. Perhaps he was referring to the total amount of dollars passed to heirs. I could find no data to support nor refute that notion.

Second, even if the statement is true, it is irrelevant. Given that THE PURPOSE of life insurance is to pass assets on to heirs, that's hardly an argument to buy life insurance for some reason besides the death benefit. As I've always said, if you want a life long death benefit that gradually increases throughout your life, then a whole life insurance policy is a great way to get that (although a guaranteed universal life policy can provide a level life long death benefit at about half the price and is probably a better solution for those who really need a permanent death benefit). Bear in mind that you are likely to leave a larger inheritance by investing in stocks and real estate than buying life insurance due to the higher returns, and those assets, just like life insurance, provide a tax-free inheritance to your heirs. Life insurance only provides a larger inheritance if you die well before your life expectancy.

This one confuses a lot of people and they get really mad when they realize how whole life insurance works. They mistakenly believe that they get a death benefit for their heirs AND a separate “cash value” investment type account that they can use themselves or leave for their heirs. What they do not realize is these two pots of money are one and the same. That which you use for yourself does not get passed on to your heirs. When they discover this fact, they feel like the insurance company is stealing a bunch of money from them and their heirs.

In reality, when you borrow against your life insurance policy, you are borrowing against your death benefit. When you die, your heirs get the death benefit minus any outstanding loans. The amount of the outstanding loans, of course, can never be more than the cash surrender value of the policy, which gradually grows to an amount very close to the death benefit at your life expectancy. So really the cash value just tells you how much of the death benefit you can borrow at any time. You can either borrow this pot of money (death benefit/cash value/surrender value) and spend it yourself, surrender the policy and spend the money, die and leave the money to your heirs, or some combination of the above. But there isn't two pots of money. There isn't a $400K cash value and a $1M death benefit. There is just a $1M death benefit. If you spend $400K of it, your heirs only get $600K of it. So you don't get an investment AND life insurance, you get an investment OR life insurance.

Вот и все. Forty reasons for buying whole life insurance debunked. Не волнуйся; the agents who sell this stuff will come up with more. Just hang out in the comments section over the next year or two and you can watch. Whole life insurance is a product designed to be sold, not bought and the only way to win an argument with an agent trying to sell it to you is to stand up and walk away. As Upton Sinclair famously said, “It is difficult to get a man to understand something, when his salary depends on his not understanding it.” Maybe it should be called Whole LIE Insurance.

Whole life insurance is a terrible investment if you don't hold on to it to your death. Since the vast majority of people surrender their policies prior to death, it is a terrible investment for the vast majority of those who purchase it. If you want to invest in it, then you need to place a very high value on its unique aspects and not mind it's serious downsides.

The ideal purchaser of whole life insurance should:

The fact is that only a tiny percentage of the population, far smaller than the number of people who have been sold these policies historically, meets all or even most of these criteria. Whole life insurance remains a product designed to be sold, not bought.

Have more questions about life insurance and what kind of policies would be best for you? Hire a WCI-vetted professional to help you sort it out.

Agree? Disagree? Please reference which “myth” you're referring to in your comment and keep comments civil and on topic. Ad hominem attacks will be deleted.

[This updated post was originally published as a series from 2013-2019.]

The White Coat Investor may receive compensation from White Coat Insurance Services, LLC; licensed in all states including MA and DC; CA license #6009217; NY license #1758759 (exp. 6/2027); Registered address:10610 S. Jordan Gateway, #200 South Jordan, UT 84095. This does not affect the cost or coverage of insurance.

Привлечение аутсорсинговой финансовой команды внутри компании:пример из практики

План обновления Apple iPhone:хорошая ли это сделка?

Предложения кредитных карт от операторов сотовой связи

Как составить бюджет на случай непредвиденных расходов

Фондовый рынок сегодня:энергия вспыхивает, когда акции резко сокращаются